|

15 OCTOBER 2008

WAS U.N.STAFF FUND AFFECTED?

by Bernard Cocheme, CEO, UNJSPF

|

The current financial crisis initially caused by high default rates of sub-prime mortgages has significantly

affected global financial markets and seriously threatens global economic growth. Recent reports also show that

liquidity has been reduced significantly, adversely impacting credit markets and banking systems, and has resulted

in the default, takeover and nationalization of several major financial institutions. Labor markets have not been

immune to the crisis and have also begun to show signs of weakness.

This crisis is the cause of great concern among pension funds and other institutional investors around the world

where many have seen the value of their investments plummet.

The United Nations Joint Staff Pension Fund (UNJSPF) has fared better than most pension funds in weathering the

crisis; its ability to meet pension benefit payments remains fully intact. Moreover, it is important that UNJSPF

participants, beneficiaries and other stakeholders understand the various mechanisms and safeguards that have been

established over the years to protect the Pension Fund from the potential effects of volatility in the financial

markets. These mechanisms are briefly described below and respond to some relevant questions that many of you

may have.

1. How has the recent turmoil in the financial markets impacted the Fund?

There is no doubt that the recent turmoil in the global financial markets has impacted the market value of the

Fund's investment portfolio. As indicated by the Representative of the Secretary-General for the investment of the

assets of the UNJSPF in his 17 September 2008 communication, the equity markets have dropped 21.9% since the

beginning of 2008. The Fund's overall market value in the same period dropped 12.2%. Most recently at the beginning

of October 2008, the value of the Fund's portfolio (32.0 billion USD) is 10 billion US dollars lower than its

all-time high market value observed at the end of October 2007 or 9 billion lower than the market value at the

end of December 2007 (41.4 billion USD).

Throughout the existence of the Fund there have been times when market volatility has impacted negatively on the

value of the Fund's assets. However, each time the impact has been temporary and the portfolio then rebounded and

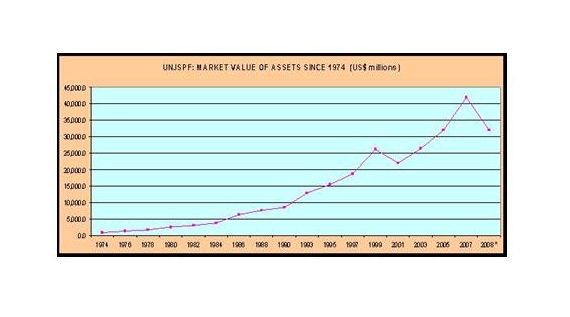

continued to grow. As illustrated in the graph below, the Fund's portfolio declined some 4 billion USD during the

financial crisis experienced from 2000-2001. However, by 2002 the market value began a long and sustained rebound

until the end of 2007. The graph illustrates the evolution of the market value of the Fund's assets as recorded

on 31 December of each year ( the value reflected for 2008 is that recorded on 8 October 2008).

It should be kept in mind that decisions affecting the investments of the Fund are made and will continue to be

made on the basis of long-term investment strategies and objectives, as decided upon by the Secretary General after

consultation with the Fund's Investments Committee and in light of observations and suggestions made by the Pension

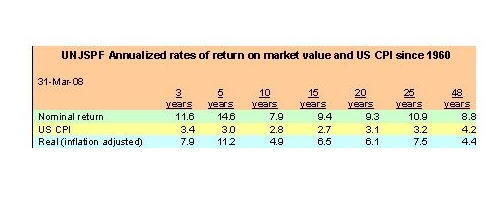

Board. As demonstrated in the table below, this long-term strategy has been very effective. For example, during the

last forty eight years (i.e. since 1960) the Fund's portfolio has been generating returns at an average rate of 4.4%

in real terms. This rate surpasses the 3.5% real rate of return objective used in the Fund's actuarial valuation.

2. Does the current market turmoil place the Pension Fund at risk?

Due to the nature of the Fund which covers participants over very long periods, during their working careers as

well as during their long retirements and even after their death (since pension payments continue to their surviving

spouses for life), this question might be best addressed if we take a look at two different time horizons: short-term

and long-term.

In the short-term, the Fund is practically unaffected by the current market conditions and I have no concerns about

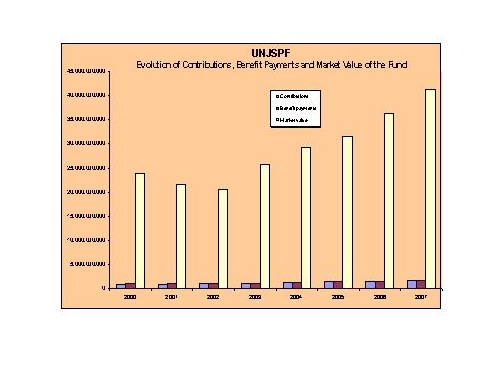

liquidity for the payment of benefits. The Fund's annual contribution income (1,672 million USD in 2007, including

48.6 million USD as a one-time transfer of assets from the International Organization for Migration after it became a

new member organization) generally covers most of the benefit payments (1,655.8 USD million in 2007).

The gap between contribution income and benefit payments is very small compared to the market value of the

portfolio (it represents much less than one percent), as may be observed in the graph above. The gap is easily

covered by the liquid portion of the portfolio. An additional source of readily available resources is dividend

and interest income. This enables the Fund to adopt a very long-term investment horizon since it is not required

to sell its equity, bond or real estate investment positions to fund short-term needs. This is obviously a very

positive feature of a fully-funded and slowly maturing defined-benefit pension scheme such as the UN Pension Fund.

Nevertheless, in the long-term high market volatility or poor continuing financial market performance may

potentially affect the Fund. The effect could be important if over several years, i.e. not weeks or months, the

long-term real rate of return of the portfolio were to fall significantly below the Fund's long-term 3.5% real

investment return considered in the actuarial projections. If this were the case, the Fund has in place sound

governance mechanisms which would enable it to take the required steps to maintain the long-term actuarial balance

and long term solvency of the Fund.

3. How may the Fund avoid potential financial difficulties?

As already mentioned, the Fund has a very good investment management track record. In addition, it has built over

the years a solid governance mechanism which closely and regularly monitors investment performance as well as the

relationship between the Fund's commitments (liabilities) and the Fund's contribution income and reserves (assets).

This ensures that an appropriate balance is maintained over the short as well as the long term.

One of the techniques employed by the Fund to ensure long-term solvency is to perform an asset liability management

study (ALM). The ALM assists the Fund in developing an optimal long-term asset allocation, in establishing an

appropriate risk tolerance philosophy and in improving its understanding of the impact of key investment and

solvency related decisions upon the financial condition and performance of the Fund. The ALM study carried out in

2007 independently tested the Fund's actuarial valuation results, the current asset allocation mix and the funding

ratio, and concluded that the Fund's actuarial valuation process is sound, the asset allocation is robust and the

Fund is stable and well- funded.

Another important element in the governance process is the role played by the Committee of Actuaries and the

Investments Committee. Both Committees are comprised of experts in their respective fields and provide independent

professional advice to the Pension Board and Secretary-General on actuarial and investment related matters.

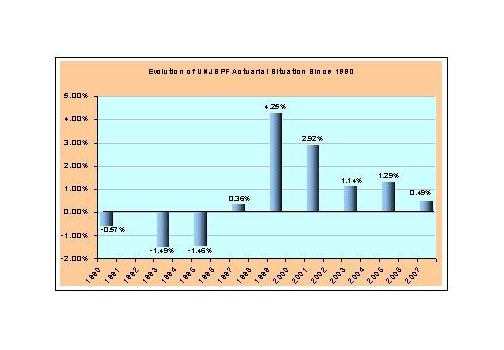

Additionally, in accordance with the Regulations of the Fund an actuarial valuation must be performed

periodically. The most recent actuarial valuation performed as at 31 December 2007 revealed the Fund's sixth

consecutive actuarial surplus (as may be observed in the graph below). This last valuation included the additional

costs of increased longevity as reflected in the Fund's revised mortality tables. These are very positive results

and provide evidence of the strong actuarial situation of the Fund.

4. Is the Fund's financial position safe?

Yes, the Fund's financial position is safe. The United Nations General Assembly has maintained over the years

four general criteria that guide the investment of the assets of the Fund. These criteria are: profitability,

safety, liquidity, and convertibility. Due to the truly international nature of the Fund it also adopted a global

diversification policy of its investments (by asset category, regions, currency, sectors, etc.). The prudent

application of these guidelines has enabled the Fund to build over the years significant reserves which are

invested under the fiduciary responsibility of the United Nations Secretary-General in well-diversified assets

with a very long-term horizon.

10 October 2008

|